Disclaimer: This article is based on the amended and draft ESRS recently published by EFRAG following the Omnibus Directive.

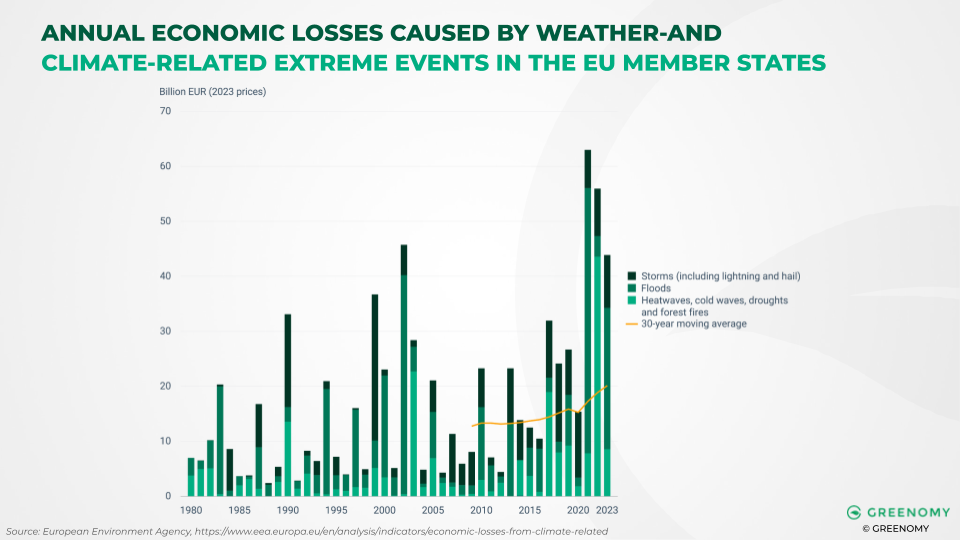

Climate change is no longer a hypothetical scenario, it is an unfolding reality that is already affecting businesses across Europe and beyond. The financial toll is striking: weather- and climate-related disasters have cost the EU more than €738 billion between 1980 and 2023, with over €162 billion in damages incurred between 2021 and 2023 alone, according to a 2024 study by EEA. What’s even more concerning is that a similar study from EEA in 2022 states that only a fraction of these losses, just 25 to 33 %, were covered by insurance.

This growing risk landscape has prompted regulatory bodies to act. Both the Corporate Sustainability Reporting Directive (CSRD) and the EU Taxonomy now require companies to assess their exposure to climate risks, and to plan adaptation measures accordingly. Central to meeting these obligations is the Climate Risk and Vulnerability Assessment (CRVA), a tool designed to help companies navigate and prepare for the physical risks of climate change.

Understanding the CRVA

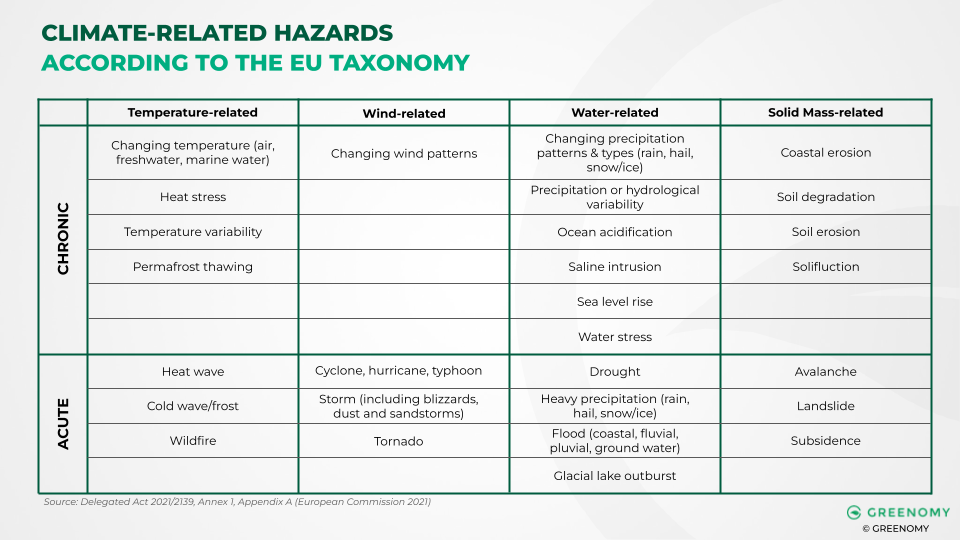

At its core, a CRVA is a structured process for evaluating how climate hazards, such as rising temperatures, changing precipitation patterns, sea level rise, and extreme weather events, could affect a company’s assets, operations, and stakeholders. It looks at both current vulnerabilities and future risks, taking into account how these might evolve under different climate scenarios and over various time horizons.

The aim is to generate a clear picture of where the organisation is most exposed, how material these risks are in financial terms, and what steps can be taken to reduce or manage them. A robust CRVA doesn’t just look inward; it also considers external factors like supply chains and infrastructure dependencies that could amplify vulnerability.

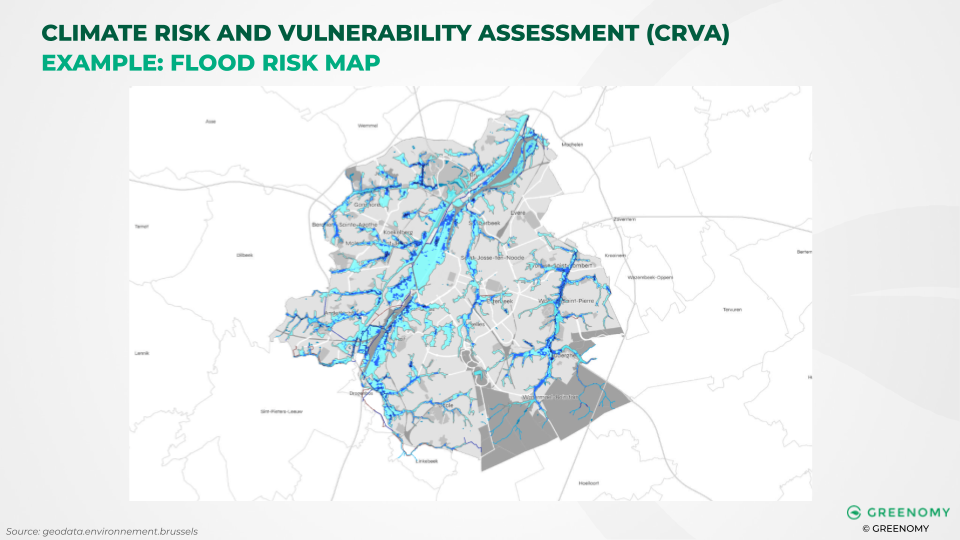

For instance, flooding is expected to be among the most costly climate risks for society. To address this, tools are available to assess such risks and integrate them into your CRVA, such as this Flood Risk Map for Brussels.

Why the CRVA Is Now a Legal and Strategic Priority

The CSRD and the EU Taxonomy differ slightly in their scope and objectives, but they converge on one point: assessing climate-related physical risks is no longer optional.

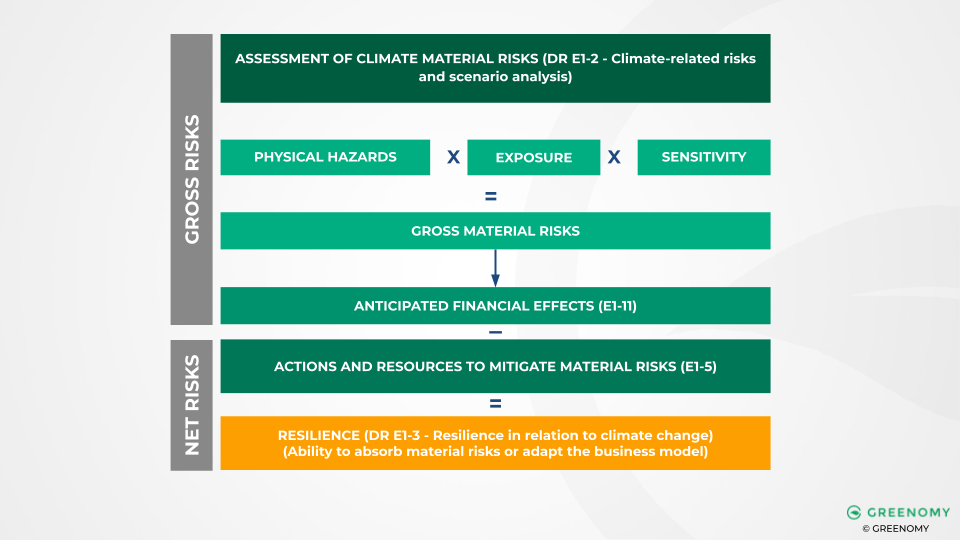

Under the EU Taxonomy, having conducted a CRVA is a mandatory condition for all eligible economic activities in order to reach the alignment. The goal here is to ensure that any activity considered sustainable is genuinely resilient to physical climate risks over its expected lifetime. The assessment is granular, focusing on specific physical assets and requiring the identification of relevant hazards, the implementation of suitable adaptation measures, and a transparent process for determining the materiality of those risks.

In contrast, the CSRD takes a broader organisational view. During the Double Materiality Assessment (DMA), companies must evaluate their exposure to physical climate risks over the short-, medium-, and long-term. These results must then be disclosed in the climate section of their sustainability report, specifically under the ESRS E1 standard. When assessing the exposure of the company’s physical assets to climate risks, the company must incorporate scenario analysis into its assessment and clearly specify the spatial coordinates and resolution applied, as these are key components of a robust CRVA.

Despite these differences, the two frameworks are closely aligned in terms of methodology. For instance, a recognised standard such as ISO 14091:2021 sets out a step-by-step methodology for conducting a robust CRVA, capturing the requirements necessary to ensure compliance with both the EU Taxonomy and the CSRD. This standard is explicitly recommended under the EU Taxonomy and was also referenced in earlier CSRD guidance prior to the Omnibus Directive. Companies are also encouraged to use financial metrics, such as potential costs from disruption or asset damage, to help evaluate the significance of each identified risk.

Integrating CRVA Across Frameworks

While the EU Taxonomy focuses on the sustainability of specific activities and the CSRD considers the company as a whole, their shared foundations make it possible, and advisable, for businesses to develop a unified approach.

This means assessing not only the most material operations and assets as required by the CSRD, but also including all physical assets linked to eligible activities under the EU Taxonomy. It also involves considering risks at the asset and activity level, differentiating between chronic and acute climate hazards, and linking those risks to financial outcomes wherever possible.

A key practical difference is that the EU Taxonomy requires assessment across the entire lifetime of an activity, while the CSRD requires analysis over defined short-, medium-, and long-term periods. Nonetheless, with careful alignment of internal processes, companies can meet the requirements of both frameworks through a single integrated risk assessment process.

Optimising the CRVA process: Greenomy’s Tips

Given all the elements of comparisons and differences, here are a few tips to optimise the process and help you ensure that the physical climate risk assessment you conduct is compliant with- and fulfils the needs of the EU Taxonomy and the CSRD.

- In addition to the most material assets and operations of the Group (as required by the CSRD), make sure that you also include all physical assets linked to eligible activities in the assessment

- Integrate the risks that are specific to the various activities taking place to a specific asset/location and differentiate them in the final risk assessment

- Use financial considerations to determine the materiality of a risk for the EU Taxonomy too

- Use the economic activity expected lifetime as the medium or long-term horizon for the CSRD

More Than a Compliance Exercise

Although the CRVA is a regulatory requirement, it also presents a strategic opportunity. It equips companies with data-driven insights into their climate exposure, enabling them to plan better, invest more wisely, and prepare for disruptions before they happen.

Financial stakeholders are paying attention too. Investors and banks are under growing pressure to disclose the climate risks present in their portfolios, and companies that can demonstrate resilience through a well-documented CRVA will be more attractive to capital providers.

In fact, adaptation can be a highly cost-effective investment. Research from the Global Commission on Adaptation shows that every €1 spent on climate adaptation can deliver between €2 and €10 in net economic benefits. This makes the adoption of adaptation solutions not only a moral or regulatory obligation, but also a sound financial decision. In some cases, implementing the solutions identified in a CRVA can even make a company eligible for favourable financing terms or green loans.

Looking Ahead

The CRVA is emerging as a cornerstone of corporate climate strategy in Europe. As the impacts of climate change accelerate and regulatory pressure grows, companies that proactively assess and address their vulnerabilities will be better positioned to weather future shocks.

Meeting the requirements of the CSRD and EU Taxonomy may seem complex, but with the right tools and approach, the process can deliver real business value, helping companies become more resilient, more transparent, and ultimately more competitive in a climate-challenged world.

.png)

.svg)