Since the European Commission announced changes to the CSRD through its Omnibus package in February, we have observed a range of responses from companies operating in the EU. Some are continuing full speed ahead, recognising that reporting ESG data will still be required or at least expected by stakeholders. Others are recalibrating their efforts, focusing on what matters most and brings value to their business. A smaller group has opted to pause or even abandon ESG initiatives altogether.

At Greenomy, we work with companies across sectors, sizes, and geographies. Drawing on this experience, we have identified a set of no-regret moves in this period of uncertainty, practical steps that help companies make meaningful progress on CSRD—and ESG in general—while easing pressure on internal teams. No-regret moves allow you to take risk-free, forward-looking actions that prepare for ESG expectations in the short, medium, and long term.

Safeguarding Against ESG Reporting Changes with No-Regret Moves

Despite the Omnibus’ proposed adjustments, the CSRD has already been transposed into national law in many EU countries. This means that compliance is still legally required unless and until local legislation is amended.

The final shape of the Omnibus proposal is also still evolving. The first part of the Omnibus package, the “Stop-the-Clock Proposal” set to delay the implementation timeline, has been adopted and should be transposed by the end of 2025. The second part of the package, the “Simplification” proposal, is still under discussion.

Various stakeholders across the EU have expressed differing views, and no consensus has been reached so far. For instance, the original proposal sets the reporting threshold at 1,000 employees, whereas the European Central Bank and several member states advocate for a 500-employee threshold. Meanwhile, the European Parliament’s JURI Committee has suggested raising it to 3,000 employees.

In parallel with potential Level 1 changes, which include modifications to the CSRD text from the scope of reporting to the type of assurance required, there is an ongoing revision of Level 2. In this case, this refers to EFRAG’s revision of the ESRS to originally achieve a 25% reduction in data points, now aiming at more than a 50% reduction. However, this process is constrained by a tight deadline, as the revised standards must be ready by end of November 2025. Keeping a close eye on national and EU-level updates ensures your company can respond appropriately and avoid missteps.

Given the current regulatory uncertainty, paired with the clear and increasing demand for ESG data from key stakeholders in the EU, companies must make a strategic decision on how to move forward with their ESG reporting. This is precisely where the concept of “no-regret moves” becomes most pertinent.

These moves serve as prudent, forward-looking steps that allow organisations to integrate ESG considerations into their business strategy to anticipate regulatory and market pressure while at the same time ensuring long-term value creation. By acting now, companies can position themselves to meet stakeholder expectations and regulatory requirements—both current and emerging—without overcommitting resources or risking misalignment with future developments.

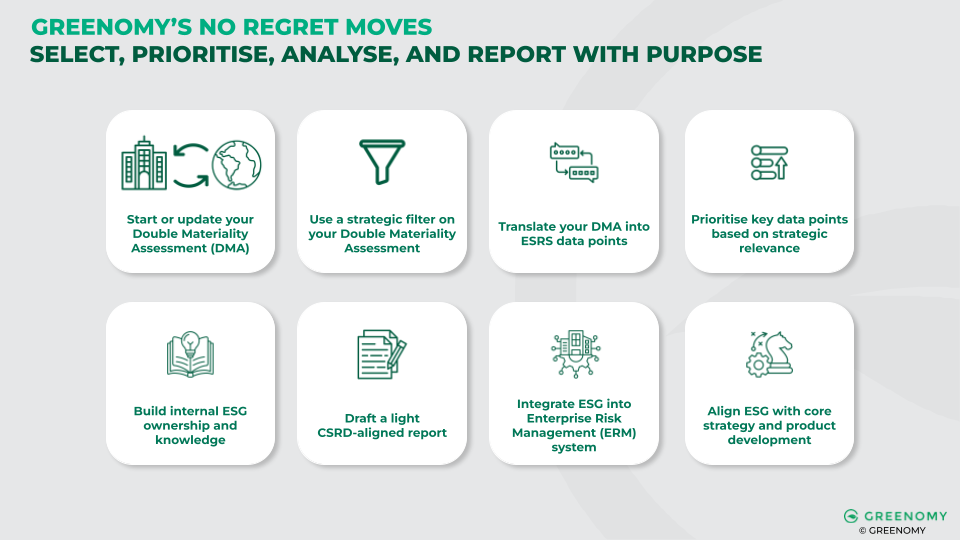

8 No-Regret Moves to Navigate ESG Reporting Uncertainty

1. Start or Update your Double Materiality Assessment (DMA)

Understand and prioritise the ESG topics most relevant to your business and stakeholders—this is foundational for any future reporting and strategy. Not only does it guide you in understanding what topics to include in your ESG report, a Double Materiality Assessment allows you to identify and manage financial risks and pinpoint areas ripe for improvement to gain operational efficiency.

What to do:

- Revisit existing assessments or initiate a new one by analysing company documentation, stakeholder input, and industry research

- Prioritise topics using a structured, documented methodology aligned with ESRS—the official methodology is out there, you might as well use it for comparability reasons

2. Use a Strategic Filter on your Double Materiality Assessment

Once your DMA has been conducted, you likely have a long list of sustainability topics identified as material across short-, medium-, and long-term horizons. This serves as your first filter for prioritising ESG topics for reporting. Apply a second strategic filter by reviewing these topics through a business lens: considering your current resources, capabilities, and budget, where can you realistically start?

What to do:

- Review your material topics through operational and resource constraints to assess feasibility

- Build a phased ESG roadmap that sequences implementation based on impact and capacity

3. Translate your DMA into ESRS Data Points

Once priority topics are identified, the next step is translating them into the relevant ESRS disclosure requirements. Each material topic links to specific data points and reporting obligations. Mapping this early on clarifies what data needs to be collected, avoiding the burden of over-reporting on ESG topics that cannot be linked to material financial effects your company is facing or the material impact the company has on its environment.

What to do:

- Map each material topic to the corresponding ESRS standard and data points by reviewing the content of the CSRD. Note that a material topic will be linked to several data points

- Assign internal owners for each topic to prepare for structured data gap analysis

4. Prioritise Key Data Points Based on Strategic Relevance

Once data points are identified, conduct a first prioritisation based on their strategic value. This way, you make sure that data is not only collected for compliance but also creates long-term value for the company. Focus on data that is meaningful to your business and meets the expectations of key stakeholders such as investors, customers, and business partners. The latter will ensure strong stakeholder relationships and a competitive advantage.

What to do:

- Perform an ESG benchmark within your sector to understand which datapoints offer a competitive advantage.

- Engage key internal stakeholders - strategy, finance, operations, etc. - to collectively determine which datapoints deliver the most business value.

For example, a construction company might benefit from calculating product-level GHG emissions to differentiate in markets with high demand for sustainable materials.

5. Build Internal ESG Ownership and Knowledge

With the regulatory reporting pressure easing slightly, now is the time for companies to invest in building internal ESG knowledge and ownership across functions. The approval of the “Stop-the-Clock Proposal” offers valuable additional time to organise and train your internal teams, clarifying roles and responsibilities, particularly within finance, operations, legal, and HR. This not only improves readiness for future compliance but also strengthens long-term resilience and accountability.

What to do:

- Assign ESG topic owners, internal experts on specific ESG matters, across relevant departments

- Provide targeted training on CSRD and ESRS basics to build internal understanding

- Set up a cross-functional ESG working group to coordinate efforts and drive progress

6. Draft a Light CSRD-Aligned Report

With more time available, you can seize the opportunity to pilot a simplified, internal CSRD-aligned report. This dry run helps build reporting capacity, test internal processes, and identify data or knowledge gaps—all without the external pressure of formal disclosure. It is a practical way to prepare for future obligations while reinforcing internal alignment.

What to do:

- Select a few key ESG data points based on previous filtering for a focused pilot

- Test data collection practices and reporting tools by simulate reporting on the select set of data points

7. Integrate ESG into the Enterprise Risk Management (ERM) System

ESG risks—ranging from climate change to regulatory shifts and social unrest—can significantly impact business performance. Embedding ESG into a company’s ERM framework ensures these risks are systematically identified, assessed, and managed alongside traditional financial and operational risks. Beyond improving resilience and anticipation of disruption, this conveys strong risk governance to investors, regulators, and auditors.

What to do:

- Include ESG risks (e.g. climate transition, supply chain ethics, water stress) in enterprise risk registers

- Conduct scenario analyses (e.g. physical risk under 2°C/4°C pathways, carbon pricing stress tests)

- Assign risk ownership and define ESG-specific mitigation plans

8. Align ESG with Core Strategy and Product Development

ESG should be a catalyst for innovation—not a compliance burden. Embedding sustainability within your business strategy helps future-proof the organisation and can support gaining a competitive edge or unlocking new markets. This positions the company as an advocate for sustainable growth, driving for long-term value creation while attracting sustainable finance and talent.

What to do:

- Embed ESG in strategic planning processes and capital allocation decisions

- Use ESG insight gathered through ESG reporting (e.g. lifecycle data, circularity metrics) to inform product and service innovation

- Evaluate investment opportunities based on environmental and social impact potential

Staying Proactive During ESG Uncertainty with No-Regret Moves

In a landscape marked by regulatory ambiguity and shifting timelines, companies may be tempted to delay ESG action. However, the direction of travel is clear: stakeholders, regulators, and investors are moving toward greater sustainability accountability, and the foundational elements of CSRD are here to stay. This is why “no-regret moves” offer a compelling path forward.

By taking proactive steps today—such as refreshing your Double Materiality Assessment, embedding ESG into strategic and risk management processes, piloting internal reporting, and building internal ownership—you lay the groundwork for future compliance and long-term value creation. These actions not only keep you aligned with likely future requirements, but also unlock internal efficiencies, improve stakeholder trust, and support innovation.

At Greenomy, we have seen firsthand how organisations that don’t wait to get started are better equipped to meet tomorrow’s expectations with agility and confidence. No-regret moves are not just about checking regulatory boxes—they are about building ESG maturity in a way that is efficient, phased, and integrated into your business. The time to act is now, and the moves you make today will shape your sustainability story for years to come.

.png)

.svg)